Introduction

Google—officially known as Alphabet Inc.—stands as one of the world’s most influential technology companies and a cornerstone holding in many investment portfolios. Whether you’re a seasoned investor evaluating your tech exposure or a beginner exploring your first stock purchase, understanding Google stock requires more than checking a price ticker. It demands a deep dive into the company’s fundamentals, market position, growth catalysts, and the risks that could reshape its trajectory.

In 2025, Google stock presents a compelling paradox. On one hand, the company dominates digital advertising, controls the world’s largest search engine, and is aggressively positioning itself as an AI leader. On the other hand, regulatory headwinds, competitive threats, and valuation concerns raise legitimate questions about whether Alphabet’s best days are behind it.

This comprehensive guide walks you through everything you need to know about Google stock—from its financial health to investment strategy recommendations—so you can make an informed decision aligned with your financial goals.

Table of Contents

- What Is Google Stock? Understanding Alphabet Inc.

- GOOGL vs. GOOG: Which Stock Should You Buy?

- Google’s Business Model & Revenue Streams

- Financial Performance & Key Metrics

- AI Strategy & Competitive Positioning

- Valuation Analysis: Is Google Stock Overpriced?

- Investment Risks & Regulatory Concerns

- Dividend Policy & Shareholder Returns

- Price Targets & Expert Forecasts

- How to Buy Google Stock

- Investment Strategy: Is Google Right for You?

- FAQ

What Is Google Stock? Understanding Alphabet Inc.

The Company Behind the Stock

Google operates under the parent holding company Alphabet Inc., created in 2015 as a corporate restructuring that separated Google’s core business from its experimental ventures (known as “Other Bets”).

Key Facts:

- Founded: 1998 by Larry Page and Sergey Brin

- Headquarters: Mountain View, California

- Stock Tickers: GOOGL (Class A, with voting rights) and GOOG (Class C, without voting rights)

- Market Cap: ~$1.7 trillion (as of 2025)

- Employees: 190,000+ globally

What Makes Google Valuable?

Google’s dominance stems from several interconnected strengths:

Search Engine Supremacy: Google controls approximately 90% of the global search market. This dominance translates directly into advertising revenue, as billions of users conduct searches daily across desktop, mobile, and voice platforms.

Advertising Powerhouse: Through Google Ads and the Google Display Network, the company captures roughly 28% of all global digital advertising spend. This creates a self-reinforcing cycle: more users → more data → better targeting → higher advertiser ROI → increased prices.

Ecosystem Integration: Android (controlling 70% of global mobile OS market share), Chrome, Gmail, Google Drive, and YouTube create a comprehensive ecosystem that keeps users engaged and provides rich behavioral data for ad targeting.

YouTube Dominance: With 2.5 billion logged-in users monthly, YouTube is the world’s second-largest search engine and a major advertising platform generating over $30 billion in annual revenue.

Cloud Infrastructure: Google Cloud Platform competes with Amazon Web Services and Microsoft Azure, representing a high-growth, high-margin business segment.

GOOGL vs. GOOG: Which Stock Should You Buy?

When investing in Google, you’ll encounter two ticker symbols, and understanding the distinction is crucial.

Class A Shares (GOOGL)

- Voting Rights: 10 votes per share

- Ownership Structure: Held primarily by founders and early investors

- Liquidity: Lower trading volume than Class C

- Price: Approximately 10x higher than Class C shares (proportional to voting premium)

- Practical Reality: Less accessible to retail investors due to high share price

Class C Shares (GOOG)

- Voting Rights: No voting rights

- Ownership: Widely held by institutions and retail investors

- Liquidity: Higher trading volume, easier to buy/sell

- Price: Approximately 1/10th of Class A shares

- Accessibility: More practical for most individual investors

The Verdict

For most investors, GOOG (Class C) is the better choice. The voting premium embedded in GOOGL shares (typically 5-10% in value) isn’t worth paying for unless you specifically value governance control—which is irrelevant for passive investors. Class C shares offer superior liquidity, lower transaction costs, and identical economic participation in Alphabet’s profits and growth.

Recommendation: Buy GOOG unless you have specific governance preferences or substantial capital requiring Class A voting control.

Google’s Business Model & Revenue Streams

The Diversified Alphabet Model

Alphabet’s organizational structure divides operations into two primary segments:

Google (Core Business):

- Google Search & advertising

- YouTube

- Chrome browser

- Android OS

- Google Cloud

- Hardware (Pixel phones, Nest devices)

- Other ventures (Maps, Drive, Workspace)

Other Bets (Experimental Initiatives):

- Waymo (autonomous vehicles)

- Verily (life sciences)

- Calico (aging research)

- Wing (drone delivery)

- X Development (moonshot factory)

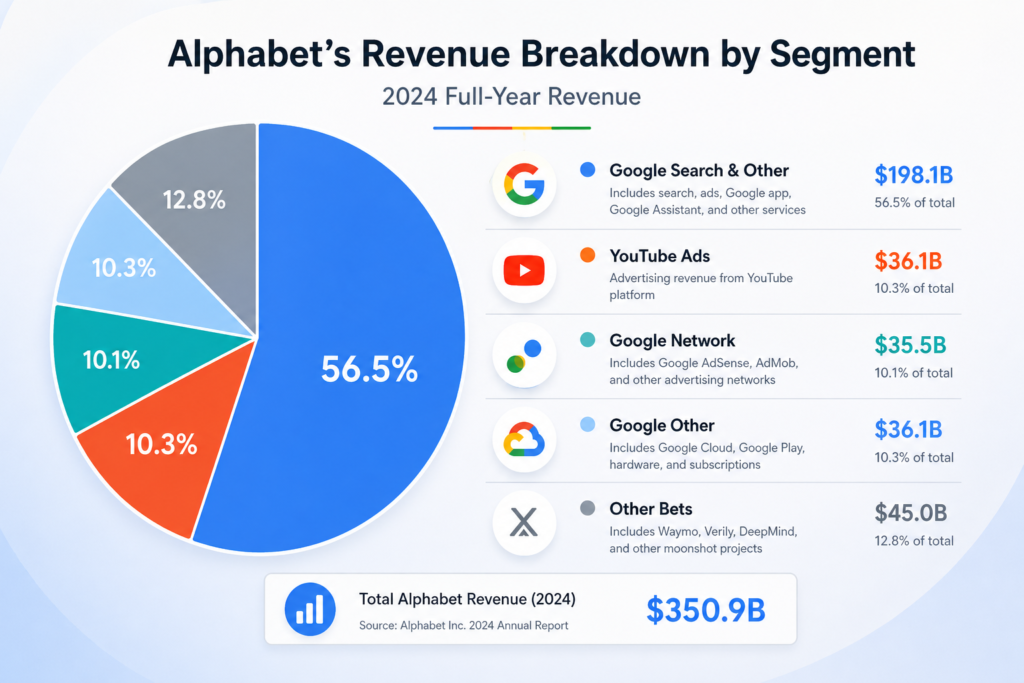

Revenue Breakdown: Where the Money Flows

| Segment | 2024 Revenue | % of Total | Growth Rate |

|---|---|---|---|

| Google Search | $76.5B | 57% | 9% YoY |

| YouTube | $31.5B | 23% | 12% YoY |

| Google Network | $27.3B | 20% | 8% YoY |

| Google Other | $11.2B | 8% | 35% YoY |

| Cloud | $13.1B | 10% | 26% YoY |

| Other Bets | $1.2B | 1% | -5% YoY |

The Advertising Dependency Problem

Here’s the critical reality: Google’s business is overwhelmingly dependent on digital advertising. Approximately 80% of Alphabet’s revenue comes from advertising, creating concentration risk.

What This Means:

- Economic downturns directly impact advertiser spending

- Shifts in consumer behavior (privacy regulations, AI-powered search changes) threaten core revenue

- Regulatory constraints on data collection endanger the targeting advantage that makes Google ads valuable

Financial Performance & Key Metrics

Revenue & Earnings Growth

Google has demonstrated consistent financial performance despite market turbulence:

2024 Performance Highlights:

- Total Revenue: $307.4 billion (+13% YoY)

- Operating Income: $88.3 billion (+20% YoY)

- Net Income: $59.9 billion (+34% YoY)

- Operating Margin: 28.7% (up from 26.1% in 2023)

- Free Cash Flow: $73.8 billion

Key Takeaway: Google’s profitability is exceptional. The company converts nearly 30 cents of every revenue dollar into operating profit—a testament to advertising’s scalability and the platform’s pricing power.

Earnings Per Share (EPS) Trajectory

| Metric | 2022 | 2023 | 2024 | 2025E |

|---|---|---|---|---|

| EPS | $5.60 | $5.97 | $8.29 | $9.45 |

| EPS Growth | -31% | 6.6% | 38.9% | 13.9% |

The 2023-2024 recovery represented a powerful comeback from 2022’s advertising recession, driven by cost discipline (the 2023 layoffs) and renewed advertiser confidence.

Return on Invested Capital (ROIC)

Google’s ROIC hovers around 18-20%, significantly above the cost of capital (8-10%). This indicates the company creates genuine shareholder value and can efficiently deploy capital into growth initiatives.

Cash Generation & Balance Sheet Strength

Cash Position (2024):

- Cash & equivalents: $110.9 billion

- Long-term debt: $13.2 billion

- Net cash position: $97.7 billion

This fortress balance sheet provides:

- Flexibility for strategic M&A

- Ability to weather economic downturns

- Capital for AI R&D investments

- Potential for increased shareholder returns

AI Strategy & Competitive Positioning

The Inflection Point: Google’s AI Transformation

In 2024-2025, Google shifted from search-engine operator to AI infrastructure provider, a strategic pivot that could reshape its competitive position and growth trajectory.

Key AI Initiatives

1. Gemini (AI Assistant & Model)

- Launched as the successor to Bard

- Integrated into Gmail, Docs, Slides, and YouTube

- Powering AI-driven ad targeting and copywriting suggestions

- Competing directly with OpenAI’s ChatGPT and Microsoft’s Copilot

2. Google DeepMind

- Breakthrough in AlphaFold (protein folding AI)

- Language model research and development

- Potential pharmaceutical and scientific applications

3. Cloud AI Services

- Vertex AI platform for enterprise AI model deployment

- Competitive threat to AWS and Azure

- High-margin SaaS model with strong growth (40%+ YoY)

4. Search Generative Experience (SGE)

- AI-powered search summaries that may cannibalize traditional search advertising

- Double-edged sword: improves user experience but could reduce click-through rates on ads

The Competitive Landscape

| Company | AI Strength | Cloud Business | Search Dominance |

|---|---|---|---|

| Strong (Gemini, DeepMind) | Growing ($13.1B) | Dominant (90%) | |

| Microsoft | Very Strong (GPT partnership) | Dominant ($80B+ Azure) | Minor (3%) |

| Amazon | Moderate (Bedrock, SageMaker) | Dominant ($85B+ AWS) | Minimal |

Analysis: Google possesses AI research parity with Microsoft and OpenAI, but Microsoft’s distribution advantage through Office 365 and Azure creates competitive risk. Google’s search monopoly is its strongest asset but faces existential threat if AI fundamentally changes how users find information.

Valuation Analysis: Is Google Stock Overpriced?

Current Valuation Metrics (2025)

| Metric | Tech Sector Avg | S&P 500 Avg | |

|---|---|---|---|

| P/E Ratio | 26.3x | 28.1x | 22.4x |

| PEG Ratio | 1.95 | 2.10 | 1.80 |

| Price-to-Sales | 6.8x | 7.2x | 2.5x |

| Price-to-Book | 6.4x | 8.1x | 3.2x |

| EV/EBITDA | 18.2x | 19.5x | 15.2x |

The Valuation Verdict

Google is fairly valued, not overpriced. The key insights:

Supporting the Valuation:

- EPS growth of 14-15% annually justifies a premium multiple

- 20%+ free cash flow margins are exceptional

- Cloud business growing 26%+ with improving margins

- Strong competitive moat around search and advertising

Concerns:

- Not cheap relative to the broader market

- Growth deceleration from 30%+ peaks of prior decades

- Regulatory risks could impact margins

- Advertising recession could quickly erode profitability

Fair Value Assessment: At current levels ($180-$190 per share for GOOG), Google offers fair value with moderate upside potential, not a screaming bargain. Conservative valuations suggest 15-20% upside over 2-3 years; bull cases project 30-40% upside if AI monetization accelerates.

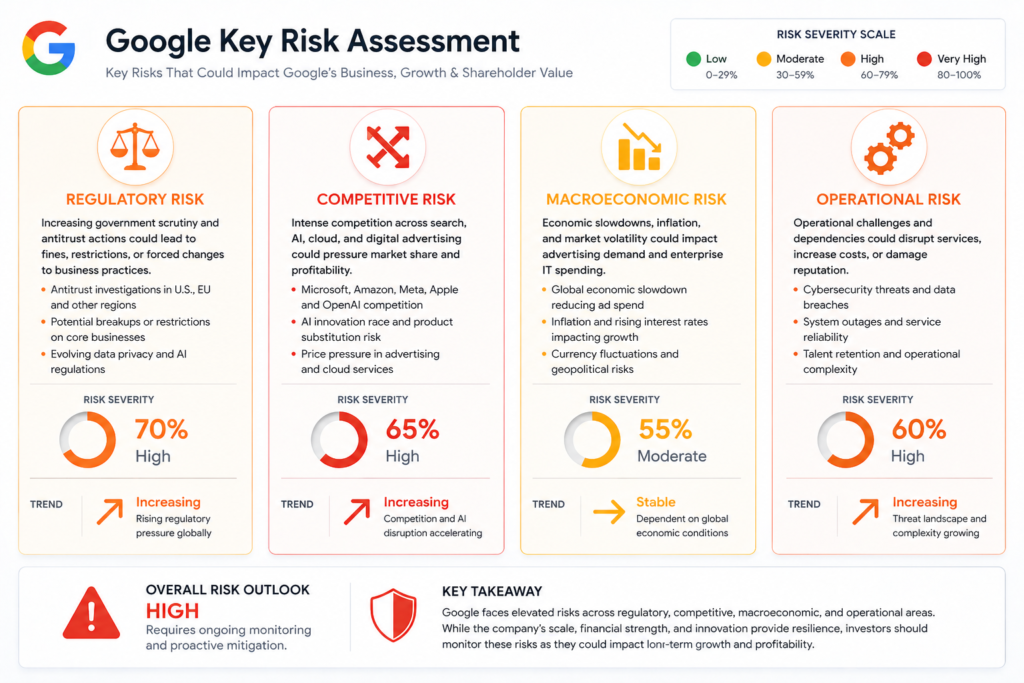

Investment Risks & Regulatory Concerns

The Regulatory Headwinds

1. U.S. Antitrust Action

In October 2024, a federal judge ruled that Google’s search monopoly violated antitrust law. The implications:

- Potential Remedies: Breaking up Google Search, preventing Android preferential treatment, or forcing licensing of search technology

- Timeline: Appeals could extend 2-4 years, but uncertainty itself creates risk

- Financial Impact: A worst-case breakup could reduce market cap by 20-30%, but near-term execution is uncertain

- Probability Assessment: Moderate probability of significant remedies; very low probability of near-term forced breakup

2. EU Digital Markets Act (DMA)

The EU designated Google as a “gatekeeper,” requiring:

- Interoperability with third-party services

- Data sharing restrictions

- Search result neutrality

Impact: Ongoing compliance costs and potential revenue headwinds in EU markets (15-20% of revenue).

3. Privacy Regulation & Data Restrictions

- GDPR, CCPA, and emerging privacy laws limit behavioral data collection

- Loss of third-party cookies diminishes ad targeting precision

- Cookie deprecation may reduce advertiser ROI on Google Ads

Operational & Competitive Risks

AI Disruption to Core Search Business

- If LLMs become primary information sources, users may bypass Google Search

- Search Generative Experience cannibalization is a real threat

- “Zero-click searches” and direct LLM answers could reduce ad inventory

Competitive Threats

- OpenAI/Microsoft partnership creating viable GPT-powered search alternative

- Apple’s search engine investment (if realized) could impact iOS query volume

- TikTok and emerging platforms capturing younger demographics

Macro Risks

- Economic recession reducing advertising budgets

- Ad fraud and bot traffic affecting advertiser trust

- Key talent departure to AI startups or competitors

Dividend Policy & Shareholder Returns

Alphabet’s Capital Allocation Strategy

Google does not pay a dividend—a deliberate choice that reflects the company’s investment priorities.

Why No Dividend?

- Aggressive Growth Investing: Capital is deployed into R&D, infrastructure, and strategic M&A

- Tax Efficiency: Shareholders receive returns through stock appreciation (taxed only upon sale) rather than dividend income (taxed annually)

- Financial Flexibility: Preserves optionality for major acquisitions or market downturns

- Reinvestment Philosophy: Management believes capital is better deployed into AI, cloud, and innovation than returned as dividends

Share Buyback Program

Instead of dividends, Google repurchases shares:

2024 Buyback Activity:

- Shares Repurchased: ~37 million shares (~$7 billion)

- Cumulative Buyback Authorization: $110 billion (ongoing)

- Impact: Reduces share count, boosting EPS

Analysis: Share buybacks at current valuations offer limited uplift (maybe 1-2% annual EPS accretion), but are cheaper than buybacks at $150 levels. This is a neutral-to-slightly-positive capital allocation decision.

What This Means for Income Investors

Verdict: Google is not suitable for dividend-seeking investors. If you need current income, consider dividend-paying stocks or ETFs. For total-return investors seeking capital appreciation, Google’s buyback strategy is acceptable but not exceptional.

Price Targets & Expert Forecasts

Wall Street Consensus (2025)

| Institution | Price Target | Upside Potential | Rating |

|---|---|---|---|

| Goldman Sachs | $220 | +22% | Buy |

| Morgan Stanley | $210 | +17% | Overweight |

| JP Morgan | $200 | +11% | Neutral |

| Barclays | $195 | +9% | Equal-Weight |

| Bernstein | $185 | +3% | Market-Perform |

Consensus Target: $200 (~11% upside)

Bull Case Scenario

Price Target: $250-280 (39-56% upside)

Assumptions:

- Successful AI monetization through Gemini and Cloud AI Services

- Cloud business reaches $30B revenue with 25%+ operating margins

- Regulatory remedies less severe than feared

- EPS growth accelerates to 18%+ through 2028

- Multiple expansion due to AI narrative

Probability: 25-30%

Base Case Scenario

Price Target: $190-210 (6-17% upside)

Assumptions:

- 12-15% annual EPS growth through 2028

- Cloud reaches $25B with improving margins

- Regulatory impact moderate but manageable

- Search remains dominant with modest decline

- Multiple contracts modestly due to slower growth

Probability: 50-55%

Bear Case Scenario

Price Target: $140-160 (-22 to -11% downside)

Assumptions:

- Forced antitrust breakup or significant divestitures

- AI threatens core search business faster than anticipated

- Advertising recession in 2025-2026

- Cloud unable to compete effectively

- Regulatory pressures erode margins by 500+ basis points

Probability: 15-20%

How to Buy Google Stock

Opening an Investment Account

Step 1: Choose a Brokerage Platform

| Platform | Min. Investment | Fees | Best For |

|---|---|---|---|

| Fidelity | $0 | Commission-free | Comprehensive tools |

| Vanguard | $0 | Commission-free | Long-term investors |

| Charles Schwab | $0 | Commission-free | Overall best-in-class |

| E*TRADE | $0 | Commission-free | Active traders |

| Robinhood | $0 | Free-to-use | Beginner-friendly |

| Interactive Brokers | $0 | Low-cost | Advanced traders |

Recommendation for most investors: Fidelity or Charles Schwab offer the best combination of zero commissions, research tools, and educational resources.

Step 2: Fund Your Account

- Minimum initial deposit: Typically $0-$500 depending on broker

- Funding methods: Bank transfer, wire, ACH

Step 3: Search for Google Stock

- Enter ticker: GOOG (Class C shares recommended)

- Or: GOOGL (Class A, if you prefer voting rights and have sufficient capital)

Step 4: Place Your Order

Market Order: Buys immediately at current market price

- Best for: Most investors buying standard amounts

- Risk: Price slippage if market is moving rapidly

Limit Order: Sets maximum purchase price

- Best for: Investors wanting specific entry points

- Risk: Order may not execute if price doesn’t reach your limit

Dollar-Cost Averaging Order: Splits investment into regular purchases

- Best for: Risk-averse investors trying to smooth entry

- Risk: May miss the bottom if stock surges immediately

Tax Considerations

For U.S. Investors:

- Capital gains tax: Short-term (held <1 year) taxed as ordinary income; long-term (held >1 year) taxed at preferential rates (0%, 15%, or 20%)

- Strategy: Hold at least one year to qualify for long-term capital gains treatment

- No dividend tax: Since Google doesn’t pay dividends, no annual tax drag

For International Investors:

- Tax treatment varies by country

- Consult a local tax professional for specific guidance

Investment Strategy: Is Google Right for You?

Google Stock for Different Investor Types

Growth Investors

- Verdict: MODERATE FIT ✓

- Why: Slower growth (12-15%) than pure growth stocks, but more stable

- Strategy: Pair with smaller, faster-growing tech companies for portfolio balance

Value Investors

- Verdict: MODERATE FIT ✓

- Why: Not cheap, but offering fair value with strong fundamentals

- Strategy: Dollar-cost average into positions; use dips below $170 as buying opportunities

Income Investors

- Verdict: POOR FIT ✗

- Why: No dividend; buybacks offer minimal income

- Alternative: Seek dividend-paying software or telecom stocks

Index Investors

- Verdict: EXCELLENT FIT ✓✓✓

- Why: Core holding in S&P 500, Nasdaq, tech ETFs; provides diversified tech exposure

- Strategy: Buy through ETFs (SPY, QQQ, VGT) for automatic rebalancing and lower costs

Conservative/Risk-Averse Investors

- Verdict: MODERATE FIT ✓

- Why: Large-cap stability, but regulatory/competitive risks exist

- Strategy: Limit to 3-5% of portfolio; avoid leveraged/margin purchases

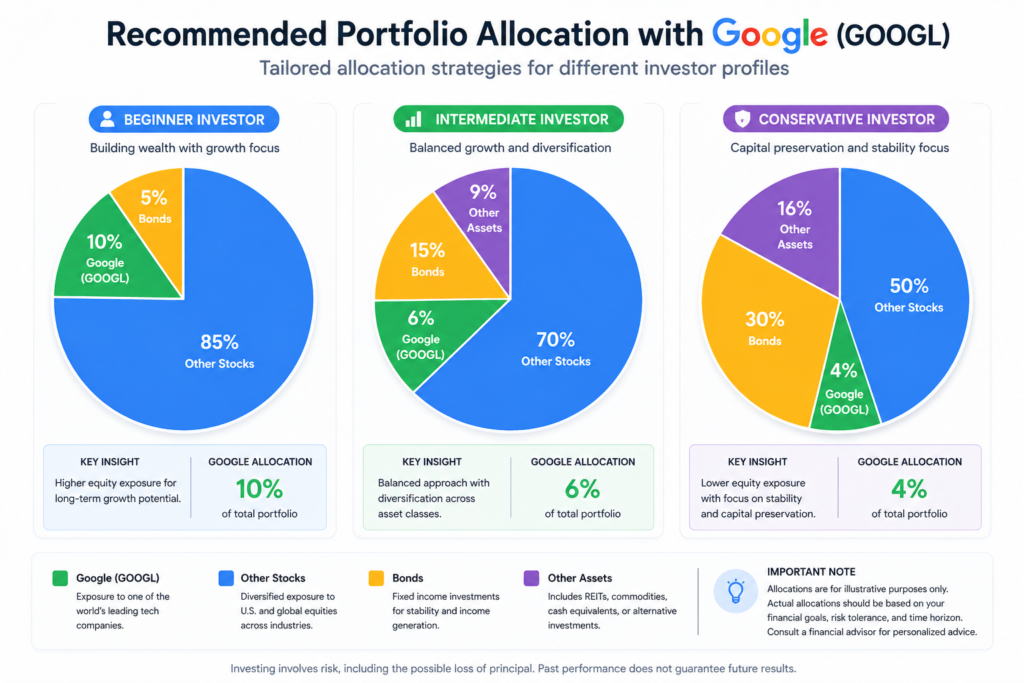

Recommended Portfolio Allocation

Beginner Investor (Ages 25-35, 20+ Year Horizon)

- Google/Alphabet: 8-12% of tech allocation

- Total tech allocation: 30-35% of portfolio

- Total stock allocation: 85-90% of portfolio

Intermediate Investor (Ages 35-50, Mixed Time Horizon)

- Google/Alphabet: 5-8% of tech allocation

- Total tech allocation: 20-25% of portfolio

- Total stock allocation: 65-75% of portfolio

Conservative Investor (Ages 50+, Shorter Horizon)

- Google/Alphabet: 3-5% of tech allocation

- Total tech allocation: 10-15% of portfolio

- Total stock allocation: 40-60% of portfolio

Buy, Hold, or Avoid?

Current Recommendation: HOLD / SMALL BUYING OPPORTUNITY

Rationale:

- ✓ Fairly valued, not overpriced (potential 10-15% upside)

- ✓ Strong competitive moats and financial fundamentals

- ✓ Positioned well in AI race

- ⚠ Regulatory risks creating near-term uncertainty

- ⚠ Growth deceleration from past decades

- ⚠ Advertising recession possible in 2025-2026

Action Plan:

- Current holders: HOLD; don’t sell due to short-term concerns

- Prospective buyers: INITIATE small positions; accumulate on weakness below $170

- Aggressive traders: Consider selling covered calls for income, or buy put options to protect downside

Conclusion

Google stock represents a high-quality business trading at fair value in 2025. The company dominates search, operates a profitable advertising empire, and is positioning itself as an AI leader. Yet regulatory headwinds, competitive threats, and the challenge of maintaining growth are legitimate concerns.

For most investors, Google stock merits a position as a core holding in a diversified portfolio—either directly or through index funds. The risk/reward profile offers moderate upside (10-20% over 2-3 years) with manageable downside if you have a multi-year investment horizon.

Key Takeaways:

- Buy GOOG (Class C shares) unless you specifically need voting rights

- Alphabet’s fundamentals remain strong despite headline risks

- AI represents genuine opportunity, but monetization success is uncertain

- Regulatory risks are real but unlikely to materially impair earnings near-term

- Dollar-cost averaging is prudent given near-term uncertainties

- Hold for 5+ years if purchased; avoid trading in/out based on short-term noise

Whether Google is “right” for your portfolio depends on your time horizon, risk tolerance, and portfolio construction. For long-term wealth builders, the company’s moat, scale, and cash generation make it a worthy core holding.

Frequently Asked Questions (FAQ)

Q1: Is Google stock a good investment in 2025?

A: Yes, for long-term investors. Google offers:

- Strong competitive moats (search dominance, Android, YouTube)

- Excellent financial fundamentals (28% operating margins, $74B+ free cash flow)

- Exposure to AI growth trends

- Fair valuation relative to growth

However, regulatory risks and growth deceleration mean it’s not a bargain. Fair value is $190-210 per share.

Q2: Should I buy GOOGL or GOOG?

A: Buy GOOG (Class C) unless you specifically want voting rights. Class A (GOOGL) trades at a 5-10% premium for voting control, which is wasteful for passive investors. Class C offers superior liquidity and identical economic returns.

Q3: Will Google’s antitrust case destroy the stock?

A: Unlikely in the near term. While the October 2024 ruling found Google’s search monopoly illegal, actual remedies could take 2-4 years to implement through appeals. Even in a worst-case breakup scenario, individual company values would likely exceed current Google valuation. The uncertainty itself creates risk, but existential destruction is improbable.

Q4: How does Google make most of its money?

A: Advertising represents ~80% of revenue:

- Google Search ads: 57% of total revenue

- YouTube ads: 23% of total revenue

- Google Network ads: 20% of total revenue

- Cloud, Hardware, Other: 10% of total revenue

This concentration creates risk if advertising demand declines or if AI disrupts search behavior.

Q5: Can AI disrupt Google’s search business?

A: Possibly, but not immediately. While LLMs like ChatGPT offer information directly without ads, several factors protect Google:

- Habit and scale: 8.5 billion daily searches create enormous switching costs

- AI integration: Google is integrating AI into search (SGE) rather than being disrupted by it

- Monetization: Even AI-powered search can carry ads and sponsored results

- Timeline: Any disruption is 3-5+ years away, giving Google time to adapt

Q6: What’s the difference between Google’s earnings and free cash flow?

A:

- Earnings (Net Income): $59.9B in 2024; represents profit after all expenses and taxes

- Free Cash Flow: $73.8B in 2024; represents cash available after capital expenditures

FCF is higher because capital expenditures (server hardware, data centers) are large but non-cash amortization is also substantial.

Q7: Should I buy Google stock now or wait for a dip?

A: Dollar-cost averaging is ideal given uncertainty:

- Aggressive approach: Buy 50% now, 50% if stock dips below $170

- Conservative approach: Buy 25% quarterly over 1 year

- Passive approach: Buy regularly through index funds (SPY, QQQ) without timing

Trying to time the market perfectly usually fails; consistent investment outperforms.

Q8: Does Google pay a dividend?

A: No. Google reinvests profits into growth, R&D, and share buybacks. For income investors, this makes Google unsuitable. The company prioritizes capital appreciation over current income.

Q9: What are Google’s main risks?

A:

- Antitrust: Potential forced divestitures or breakup

- AI disruption: LLMs could change how users search

- Advertising recession: Economic downturns reduce advertiser spending

- Privacy regulations: Data restrictions limit ad targeting

- Competition: Microsoft (via OpenAI), Apple, Amazon challenging various segments

Q10: How much of my portfolio should be Google stock?

A:

- Growth portfolios: 5-10% of tech allocation (8-12% of total if tech is 30%)

- Balanced portfolios: 3-6% of tech allocation (6-12% of total if tech is 20%)

- Conservative portfolios: 2-4% of tech allocation (4-8% of total if tech is 15%)

Use index funds for easier diversification rather than individual stock picking.